AppLovin (NASDAQ: APP) Analysis

Can't run from the advertisements? Then you should invest in them!

Not gonna lie. While we all hate advertisements, the business itself is insanely profitable. We have seen Meta and Google at the forefront of this Ad-volution, but we feel that the pie is big enough for small market players to rise to power too. Here is one company that we really, really admire. Hope you will like it just as much as we do.

1. Company Background and Founding

AppLovin, an advertising technology company based in Palo Alto, California, is a leading advertisement technology company with a mission to help businesses reach, monetize, and grow their global audience. From the outset in 2012, AppLovin's founders understood the difficulties developers face in marketing and monetizing apps in a highly competitive landscape. Unlike many startups, they prioritized building a strong tech foundation, focusing on hiring engineers and data scientists over sales and marketing teams.

This early focus on technology paid off. Operating in stealth mode, AppLovin attracted over 300 major brands as clients within two years. By the time they emerged in late 2014, the company was already achieving a $200 million run rate.

^^ Credit: Nasdaq

Despite a rumored $1.5 billion acquisition offer from a Chinese private equity firm in 2016, which eventually fell through, AppLovin continued to grow. The company went public on Nasdaq in April 2021. Although their stock surged from $80 to a peak of $116.09 in November 2021, it sharply declined to $9.14 by the end of 2022, following underwhelming revenue growth and a failed merger with Unity. However, the company rebounded over the next two years, achieving an impressive 37% revenue growth at 38.86B market cap, the second fastest among application software companies over $10 billion, just behind Duolingo (43% at 10.19B market cap).

Today, AppLovin is recognized for its innovative mobile app marketing and monetization solutions, trusted by app developers and advertisers globally to help grow their businesses. The platform uses AI and machine learning to solve critical challenges in the app development journey, from discovery and optimized marketing spend to maximizing user engagement and monetization.

2. Industry Insight

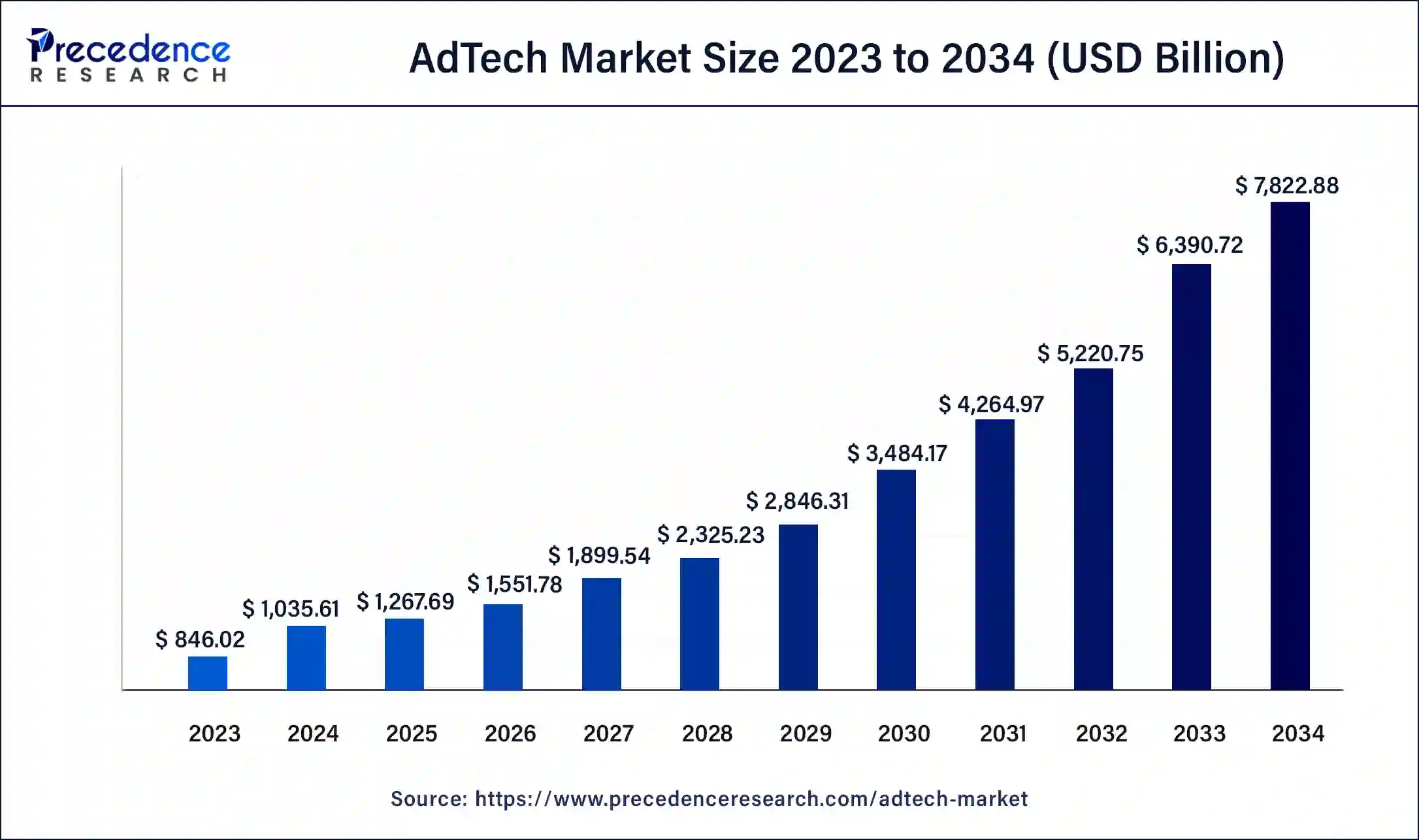

The global AdTech market is poised for rapid expansion, with an expected CAGR of 22.41% from 2024 to 2034. Programmatic advertising already accounts for over 82% of the market’s revenue in 2023, and mobile platforms, which represent 56% of this market, are fueling this growth. Applovin, with its AI-driven technologies and advanced ad targeting solutions, is uniquely positioned to take advantage of these trends, particularly as demand-side platforms (DSPs) continue to grow, enhancing real-time bidding and campaign optimization.

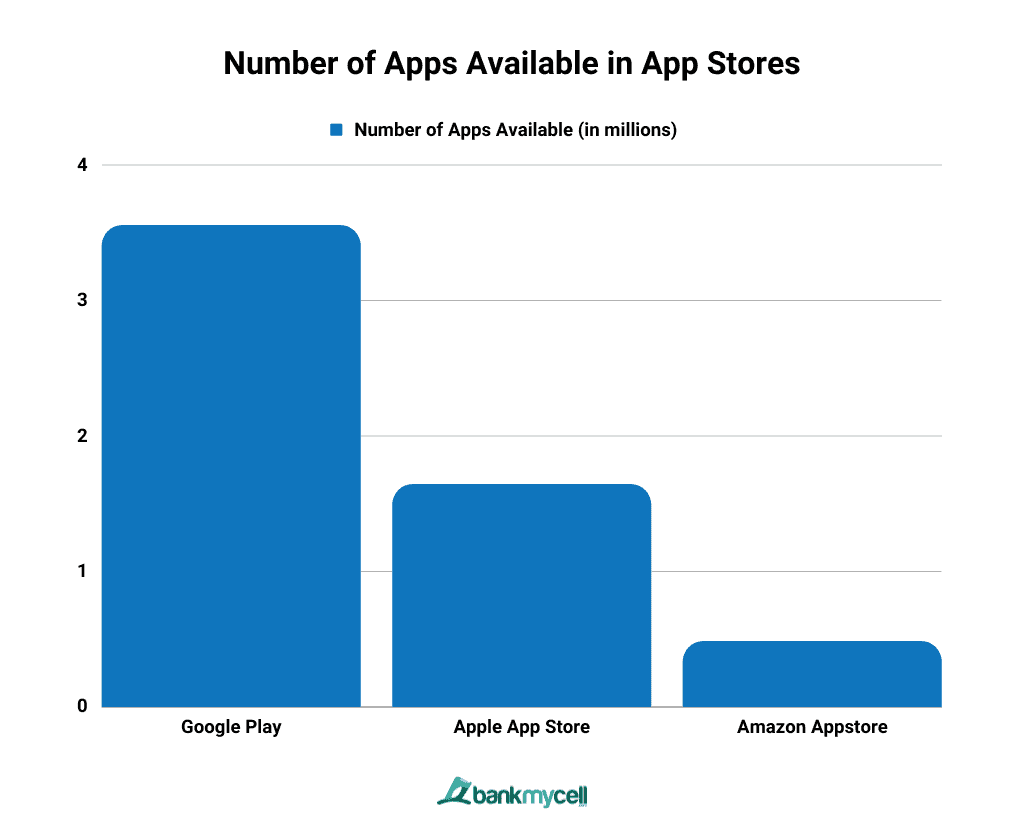

Simultaneously, the mobile app industry has experienced explosive growth, becoming an integral part of daily life for billions of users. Yet, this growth has led to significant challenges for developers. Market saturation, with over 8.93 million apps available on over 300 app stores globally, makes standing out increasingly difficult. Furthermore, SensorTower estimated in 2019 that 80% of all mobile app downloads are concentrated among just 1% of developers. Most developers also face challenges in marketing and monetization, lacking access to the sophisticated tools necessary for effective user acquisition and revenue generation.

The mobile gaming segment, a fast-growing sector within this ecosystem, represents both opportunities and challenges for developers and platforms like Applovin. As the industry evolves, advanced marketing, monetization, and analytics tools are becoming critical for success. Applovin’s platform, focused on mobile app-based marketing and video-centric ads (which are projected to grow at a 24% CAGR), positions it as an essential partner for app developers seeking to navigate this competitive landscape. By tapping into fast-growing regions like Asia Pacific, Applovin has the opportunity to further scale its data-driven solutions and support a broader range of developers in overcoming market saturation and revenue generation challenges.

3. Product Summary

AppLovin's flagship product is its comprehensive, AI-powered software platform. For the other half of the business, AppLovin also operates a diverse portfolio of owned mobile apps. This unique positioning has enabled AppLovin to drive success for both its clients and the company itself. With continued push into R&D, AppLovin’s own mobile apps would be able to benefit from enhancement to its advertising platform.

The platform offers a suite of advanced tools designed to help advertisers manage, optimize, and scale their profit model. The comprehensiveness of the full stack service helps individuals or small businesses to cover their lack of marketing manpower and budget.

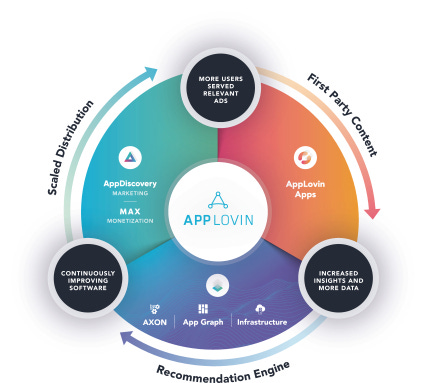

At the center of this platform is AppDiscovery, an AI-powered marketing solution driven by AXON, which connects advertisers with the right users, maximizing campaign performance through rapid and personalized ad placements.

Another key product, MAX, is a bidding technology that optimizes the value of publishers' ad inventory by running real-time competitive auctions for advertisement placement, resulting in higher returns for publishers while automating many manual processes.

Adjust, the company’s measurement and analytics platform, provides marketers with valuable insights into app performance and user engagement, allowing them to scale their advertising efforts effectively. (Acquired in April 2021)

AppLovin has also expanded into the connected TV space through Wurl, a platform that distributes streaming video content and helps companies grow their audience while maximizing ad revenue. (Acquired in February 2022)

In addition, AppLovin offers SparkLabs for advertisement creation, Exchange for advertisement bids optimisation (in conjunction with Max) and Array as the App management suite for mobile operators and OEMs.

AppLovin also operates a vast portfolio of over 200 free-to-play (F2P) mobile games across various genres, developed by 11 studios globally. The portfolio includes casual and card/casino games that appeal to a wide range of demographics. These games, designed to be easy to learn and play, generate predictable revenue streams and have a high level of user engagement. The studios behind these apps utilize AppLovin’s Software Platform to optimize user acquisition, in-game monetization, and scaling, ensuring that the games reach a global audience and generate high returns.

4. Business Model and Go-to-Market Strategy

AppLovin accounts for their revenue through 3 segments:

Software Platform: Fees paid by mobile app advertisers and publishers using AppLovin's Software Platform for user acquisition, monetization, and analytics.

In-App Purchases (IAP): Additional money paid by users within AppLovin's own mobile games to obtain benefits, such as in-game items.

In-App Advertising (IAA): Revenue from clients purchasing advertising inventory within AppLovin's portfolio of apps.

AppLovin's go-to-market strategy leverages its comprehensive platform to create a positive reinforcement loop:

Attract developers with effective marketing and monetization tools.

Use insights from its own apps to improve its technology and offerings.

Leverage increased scale and data to enhance its AI-powered recommendation engine.

Deliver more value to developers, attracting more users to the platform.

The software platform not only provides advertisers with the tools to maximize their marketing and monetization efforts but also fuels continuous improvements by leveraging data from its apps and global audience. This virtuous cycle enhances the performance of both AppLovin’s platform and its clients, ensuring sustainable growth and success.

5. Key Risks

Besides common risks that apply to all companies, there are a few that concern AppLovin in particular:

Reliance on Third-Party Platforms: Changes in partner platform policies (e.g., Apple or Google) or disruptions could significantly impact their operations.

Regulatory Risks: Changes in laws concerning privacy, AI, intellectual property (IP) and advertising, especially regarding data protection and the use of AI in advertising, could impact operations. AppLovin must navigate compliance in various jurisdictions, adding complexity and risk to their international operations. Additionally, managing open-source software compliance and licensing could introduce legal vulnerabilities too.

In-App Purchases (IAP) Revenue concentration: The IAP revenue segment is concentrated. In FY2023, three games, Project Makeover, Matchington Mansion and Wordscapes, represented ~15% of revenue. Based on the 6 months ended 24Q2, two games, Wordscapes and Project Makeover, represented ~10% of revenue. However, the revenue generated by Software Platform has massively increased compared to Apps revenues (inclusive of IAA), thus the impact is increasingly minimized.

Substantial Indebtedness: As of June 30, 2024, AppLovin’s outstanding indebtedness under credit facilities was $3.55 billion. The company's debt-to-equity ratio is currently at 4.32, which is relatively significant, and thus pose concerns to its liquidity during economic downturns.

6. Competitor Analysis

Since AppLovin’s revenue comes from its software platform and apps mainly, the competitors are also examined by industry. AppLovin faces competition from several key players within the AdTech and mobile app monetization ecosystem:

AdTech Platforms and Services

Digital Turbine (APPS)

Perion Network (PERI)

Magnite (MGNI)

PubMatic (PUBM)

Criteo (CRTO)

The Trade Desk (TTD)

DoubleVerify (DV)

Gaming Platforms and Developers

Unity Software (U) (parent of ironSource)

Playtika (PLTK)

Take-Two Interactive (TTWO) (parent of Zynga)

Roblox (RBLX)

Sea Limited (SE) (parent of Garena)

Electronic Arts (EA)

AppLovin’s competitive advantage lies in its all-in-one ecosystem, integrating app discovery, user acquisition, and monetization. Its software solutions, such as AppDiscovery and MAX (an advertiser-matchmaking platform), are designed to help app developers scale and optimize their user acquisition strategies across various ad networks. Furthermore, their proprietary machine learning algorithms enhance ad targeting, user engagement, and monetization outcomes for developers.

However, AppLovin faces strong competition from established giants like Unity, Google, and Meta, which have broader brand recognition and larger ad ecosystems. Unity, in particular, poses a significant challenge due to its deep integration into the gaming development lifecycle and the merger with ironSource. The competitive landscape is further intensified by the growth of programmatic ad networks and rising demand for privacy-first solutions, which AppsFlyer and Singular are focusing on.

At a stock price of $130 per share, AppLovin has a pricey valuation compared to its peers. While the P/S ratio and P/E ratio may seem high, AppLovin has the highest growth among all its competitors. (Roblox is the second highest at 29%.)

Based on our internal projections, while we expect the P/S ratio to remain high, the P/E is expected to significantly improve. Based on the past few fiscal quarters, we noticed that the software platform revenue has significantly outpaced its app-based revenue, which has allowed AppLovin to expand its margins.

Thus, despite challenges from competitors, AppLovin's strong market position and continued expansion through acquisitions suggest it is well-positioned to maintain its momentum. The company's ability to integrate and optimize its services will be crucial in navigating this competitive and evolving industry. Investors may find AppLovin's strategy to enhance its ecosystem compelling, though the competitive dynamics warrant close monitoring.

7. Financial Analysis

This section will contain a list of highlights in AppLovin’s statements that we feel are remarkable.

Firstly, AppLovin had a significant revenue increase in the quarter ending Sep 23, both at a QoQ basis and a YoY basis. It grew from 713.1M in Sep 22 quarter and 750.1M in Jun 23 quarter to 864.2M in Sep 23, an increase of 21.2% YoY and 15.2% QoQ. It subsequently continued this stellar growth rate.

AppLovin has also shown that this growth is not a result of blind drive towards customer acquisition, since it has also turned profitable over the past two years. For investors who are avoidant towards tech companies that burn cash at the cost of margins, this should come as a relief.

In continuation of the previous point, we have seen sustainable expansions of margins in AppLovin’s operating model. While the margins may not perpetually grow at this rate for too long due to the nature of the industry landscape, we believe that R&D efforts in both direction and capital invested may represent a greater return on equity (currently at 70.92%) for the investors,

As mentioned in the Key Risks section above, a relatively important concern to take note of is AppLovin’s debt at $3.55 billion, which is relatively significant to its asset value. The current debt-to-equity ratio sits at 4.32, while the debt-to-asset ratio sits at 0.67.

However, this leads to a positive note, as the main reasons for the drop in stockholder equity were the reduction in additional paid-in capital due to stock repurchases in addition to the increase in long-term debt. AppLovin has shown good faith to investor’s equity value with an expanded share repurchase program at $1.24B. At the same time, there is a reduction in the accumulated deficit, which reflects improved earnings. As far as balance sheet goes, if investors are comfortable with the debt, the company is sitting in a good spot.

For selected advanced metrics:

EV/EBITDA: 28.47

Forward PEG: 0.53

8. Conclusion

In conclusion, AppLovin's position in the AdTech and mobile app ecosystems remains robust, with its AI-driven platform, diverse portfolio, and focus on R&D fueling consistent growth. Despite facing competitive pressures from well-established players like Unity, The Trade Desk, and Google, the company's all-in-one approach to app discovery, user acquisition, and monetization provides a strong foundation for future success. Its ability to scale through proprietary machine learning and product innovation, such as AppDiscovery and MAX, creates a unique value proposition in the highly saturated mobile app industry.

The company’s recent financial performance, including significant revenue growth and an expanding software platform, underscores its ability to navigate a challenging macro environment while improving profitability. Although AppLovin's high debt levels raise concerns about liquidity during economic downturns, the firm’s proactive steps—such as share repurchases and sustained margin improvements—demonstrate sound financial management.

Looking ahead, the AdTech industry is poised for continued expansion, with programmatic advertising and mobile app-based marketing at the forefront of this growth. AppLovin’s ability to adapt to shifting regulatory landscapes, privacy concerns, and platform changes will be critical to its sustained momentum. However, its track record of innovation, combined with a disciplined approach to operational growth, suggests that AppLovin is well-positioned to capitalize on emerging opportunities and cement its leadership within the evolving digital advertising space. While challenges remain, the company’s long-term prospects appear promising, making it a compelling, if cautiously optimistic, investment opportunity.